Algorithmic marketing is defined as comprehensive guidance towards marketing automation for data scientists, and product managers as well as for software engineers by including advanced techniques of marketing implemented by advertising, retail and technology companies. In accordance with this, algorithmic marketing often helps companies decrease costs, improving efficiency and thereby maintaining proper accuracy as well as precision.

The Buy Now Pay Later Sector has the major impact of win, loss and neutral outcomes of algorithmic marketing and also includes the significant rate of advanced sales and conversion rates within e-commerce. This study includes the BNPL sector regarding analysis by focusing on Klarna AB. This context includes the outcomes of win, loss and neutral in the BNPL sector, an extension of the meeting the Pellandini-Simanyi’s criticism as well as the recommendations for this sector and for this company.

What are the outcomes (win, lose, neutral) of algorithmic marketing on consumers within the marketing system (Reference to BNPL sector)

Win

Personalised Recommendations:

Algorithmic marketing allows Klarna to assess customer behaviour and core preferences, which leads to customised recommendations about products. This can improve the shopping experience by showcasing relatable choices that are tailored to individual interests, which increases the likelihood of core purchase completion (Kotras, 2020).

Convenience and Flexibility:

BNPL services provide customers with the convenience of purchasing without any need for immediate payment (Aalders, 2023). The algorithmic approach of Klarna can develop its payment plans according to factors such as generic income, patterns of spending, and creditworthiness, which offers flexibility and eases core financial burdens for the customers.

Improved Financial Literacy:

The algorithmic tools of the business can practically educate the customers regarding their spending habits, total budgeting, and diverse financial responsibilities (Srinivasan & Sarial-Abi, 2021). By offering different insights about the payment schedules as well as potential interest charges, the customers might become more financially aware and could be able to make more informed decisions regarding their purchases.

Enhanced User Experience:

Through precise data-driven algorithms, Klarna can technically streamline the method of checkout, which decreases the friction points and enhances the overall user experience. This method can possibly lead to a higher rate of customer satisfaction and a sense of loyalty.

Top UK Assignment Samples

Lose

Debt Accumulation:

While BNPL services deliver some short-term facilities, they can also potentially lead to the issues of debt accumulation if the problem is not responsibly managed (Cook et al. 2023). Algorithmic marketing might influence impulse buying or the habits of overspending by presenting few enticing offers along with simple options of payment, that will increase financial strain for some of the customers.

Interest Charges:

Customers who fail to correctly adhere to the given payment schedules or exceed certain credit limits might incur an amount of interest charges and fees (Chen, 2022). The algorithmic approach of Klarna, while developing its payment plans, can also negatively result in some additional costs for customers who do not regularly monitor their spending patterns and payment obligations in a careful manner.

Privacy Concerns:

Algorithmic marketing technically relies on customer data to enable the system of personalised targeting alongside decision-making (Pavlidou et al. 2022). This method raises a few privacy concerns about data collection, proper storage, and usage. The customers might feel uneasy about sharing sensitive data with organisations such as Klarna, as the proposed marketing method can allow certain data breaches or misuse.

Top Dissertation Topics UK

Neutral

Market Competition:

The core strategies of algorithmic marketing are very much prevalent around the BNPL industry, with Klarna competing against other similar providers in the marketplace. While these exact strategies can possibly lead to creative product offerings as well as competitive pricing, they might also build a saturated atmosphere of the market, which makes it difficult for the customers in order to differentiate between services which are solely based on algorithmic marketing efforts (Cao et al. 2024).

Regulatory Scrutiny:

By installing the BNPL strategies, the company Klarna might face regulatory scrutiny about customer protection, clarity, and also responsible practices of lending. Algorithmic marketing practices should comply with the core regulations in order to make sure of fair and ethical treatment of the customers, through balancing innovation with certain regulatory requirements.

Customer Choice:

Algorithmic marketing can supportively encourage customer choices by presenting created options and diverse promotional offers. However, the customers finally retain the choice in order to accept or reject these exact offers as per their preferences, specific needs, and financial circumstances (Li et al. 2022). The algorithmic approach of Klarna is required to respect the concept of consumer autonomy and deliver concise information in order to support the process of informed decision-making.

After considering all the potential outcomes regarding algorithmic marketing in the BNPL industry, the actual outcomes can vary depending on numerous factors.

Positive Outcomes

Growth of Sales and Consumer Retention:

Algorithmic marketing can optimistically lead to increased amount of sales by offering customised suggestions and a smooth shopping experience (Akter et al. 2022). This method can develop customer satisfaction and loyalty, through contributing to prolonged relationships and repetitive business.

Enhanced User Experience:

By enhancing the payment plans and decreasing certain friction points, algorithmic marketing can refine the entire user experience, which makes it easier as well as more convenient for the customers to make the right purchases.

Financial Awareness:

Customers who get engaged with the algorithmic tools of Klarna might craft better financial literacy and core awareness of their spending habits, which makes more responsible financial behaviour.

Negative Outcomes

Debt Accumulation and Financial Strain:

In spite of the convenience that is delivered by BNPL services, some customers might experience the barriers of debt accumulation and financial strain if they misuse or overextend their limited credit. This way it can lead to few negative outcomes like missed payments, and a lot of interest charges, which ultimately affect the main credit score.

Privacy Concerns:

The notion of algorithmic marketing genuinely relies on customer data, which raises certain security issues about data privacy, core transparency, and ethical usage of the collected information (Liu et al. 2023). Mishandling of customer data can result in the initiation of trust issues and some potential regulatory penalties for businesses such as Klarna.

Neutral Outcomes

Market Competition:

The competitive nature of the BNPL industry primarily refers to the algorithmic marketing strategies, which are widespread among providers such as Klarna. While this procedure can lead to attractive offerings and competitive pricing, it might also introduce particular challenges in differentiating the core services according to the sole marketing tactics.

Regulatory Compliance:

Correct adherence to the regulatory requirements is very significant for associations such as Klarna in order to operate ethically as well as sustainably. The system of algorithmic marketing practices should resonate with the basic customer protection laws, certain regulations, and core standards of data privacy in order to resolve the risks and make sure of fair treatment of the customers (de Marcellis-Warin et al. 2022).

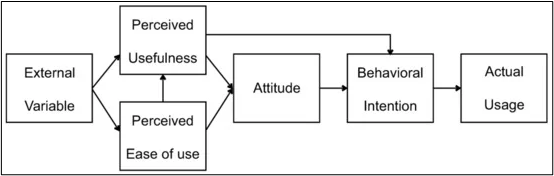

Technology Acceptance Model

Figure 1: Technology Acceptance Model

(Source: Park & Park, 2020)

Technology Acceptance Model posits that the intention of an individual in order to leverage technology is totally influenced by perceived advantages and proper ease of usage (Park & Park, 2020). In the main context of BNPL services, the acceptance of the customers and adoption of algorithmic marketing strategies can be vividly evaluated through precise TAM, as it considers factors like personalised advice, the right convenience, and beneficial user experience.

To what extent Pellandini-Simanyi’s criticism holds true in the BNPL sector

If the article authored by Pellandini-Simányi (2023), is analysed, then it can be seen that the criticism of the BNPL sector is massively true that the overall new concept of algorithmic marketing is creating and shaping cultural and economic inequalities among the people belonging to different classes. Klarna AB is a popular BNPL company operating in the market of Europe including the UK. It allows the consumers to have the benefit of flexible and convenient payment through which it can be said that they get the chance of paying later, instead of the time of purchasing their preferred items. This says that in most cases, it creates benefits for the customers.

If the customers avail of the BNPL service of Klarna AB, then they get the facility of three types of BNPL options. Those are Pay Now, Pay in 3 and Pay in 30 days (Shop and pay the Klarna way, 2024). Here in this context, it is seen that the ‘Pay Now’ option, is highly effective as with the help of this, the consumers can choose their preferred payment method even before purchasing.

Secondly, in terms of Pay in 3, it is seen that the customers are allowed to spread their cost of purchase into three significant equal interest-free instalments. In this system, the first payment is made at the time of purchasing the items by the customers, and the two remaining installments are scheduled every 30 days automatically. Thirdly, as per the ‘Pay in 30 days’ system, it is seen that the consumers are allowed to pay the costs for their purchased items within the next 30 days after the day of purchasing without any interest (How does Klarna work, 2024).

Therefore, initially, it is seen that the BNPL service like Klarna AB seems attractive and helpful for the customers. Therefore, it is seen that the entire thing is based on database marketing. As stated by Chen (2022), in this modern era, the internet has been highly matured and as a result, the frequent use of various information technologies, database technologies, database marketing and many more have been increased for the sake of making the consumers happy.

Here, the company officials use technologies to explore and identify consumer information so that they can easily understand what the consumers want to buy and what types of payment methods they prefer along with these, it helps the company officials to develop concrete relationships with their customers for understanding their psychology.

Recently, some market studies have stated that in most cases, all are effective with the help of this, it is seen that the popularity of BNPL systems is increasing in the UK and 2023, the BNPL transaction value was 33,810 USD and in 2024, it is estimated that the value would be increased to 38,761.30 USD. This means it is seen that in most cases, the value for BNPL is increasing and the experts assume that in 2029, it will reach 61,393.70 USD (De Best, 2024). Therefore, it is understood that the officials of Klarna AB utilise the database marketing system and based on this, they have been able to understand these and for this, they have adopted various flexible BNPL options for their consumers.

However, initially, it looks attractive, but inequalities are there. As an example, it can be said that this kind of marketing shapes class patterns. Mainly it creates patterns for social classes. In the context of BNPL, it can be said that since the opportunities are made based on the financial conditions of the people, it is seen that this kind of marketing defines the poor, rich and middle-class sections of the people (Pellandini-Simányi, 2023).

Here the algorithms used for analysing the classes, it is seen that the algorithms match various predictions based on different sorts of variables. In the course of this, it is also seen that the algorithms that are used for music and movie recommendations cause various taste structures and in this way, inequality occurs.

Similarly, in the path of categorising the people in the market for defining the most suitable BNPL service, it can be said that various social groups are formed. This creates inequality among the people (Pellandini-Simányi, 2023). On the other hand, it is seen that in the BNPL sector, the customers are categorised on the basis of credit scores. In this context, the algorithms that are used to provide credit scores to the customers make the scores based on belonging to them to specific social groups.

In this context, it is also seen that algorithms set some specific items to define whether any person belongs to the upper class or not (Pellandini-Simányi, 2023). As an example, it can be said that the algorithms categorise upper-class people if they have the trend to buy items that are related to updated luxury fashion trends. Due to this reason, it can be said that it creates inequalities among the people. In this context, it can be said that based on access to financial products, their class positions are determined.

The algorithms predict the future wealth and disposable income for the customers and if it is seen that according to the income level, any consumer can take loans with low interest or loans with high-interest rates (Pellandini-Simányi, 2023). Here, the consumers with the capability of taking loans with high interest rates are considered the better borrowers. This helps to deal with things like effective management of all the things.

Apart from this, it is also seen that some financial provider companies use algorithms to identify the consumer segments and make decisions on which consumers should be targeted with various kinds of customised advertisements, whom to be offered payday loans and many more. This means it is seen that people with financial capability can be considered lower class if they do not have taste in the latest fashion trends and for this, they can be denied with the effective BNPL services they want.

Recommendations to address the issues

Klarna can improve its useful strategies of algorithmic marketing by prioritising the concept of clarity and proper customer education. The application of seamless communication regarding payment terms, different interest rates, and data privacy can build a sense of trust with the consumers of Klarna.

Offering precise educational resources about the subject of financial responsibility and budget management within the official app or website of the company can technically empower the users in order to make informed decisions. Klarna must regularly update its algorithmic models in order to make sure of the right accuracy, proper fairness, and correct compliance with the base of regulatory standards, which thereby promotes some optimistic customer experiences.

Get Assignment Help for Top Subjects

Conclusion

The study has thoroughly explored the sole outcomes of installing algorithmic marketing in the BNPL sector, which is technically exemplified by the organisation of Klarna. It vividly reveals an intricate outlook of general benefits, potential risks, and the correct maintenance of basic ethical considerations. The good facilities of useful algorithmic tools can practically develop personal experiences with customised references, proper convenience of shopping, and financial literacy.

From the article of Pellandini-Simanyi, criticisms of this journal regarding discrimination and inequality are truly related to algorithmic marketing. On another note, it also poses constraining challenges like the accumulation of possible debts, core privacy concerns, as well as market saturation.

The range of success achieved by Klarna hinges on balancing these mentioned factors through the transparent level of communication, customer education, regulatory compliance, and constant enhancement of the algorithmic models. By considering and prioritising the base of ethical practices along with consumer welfare, the business Klarna can bring out some positive outcomes for both the customers and the organisation.

References

Aalders, R. (2023). Buy now, pay later: redefining indebted users as responsible consumers. Information, Communication & Society, 26(5), 941-956. https://doi.org/10.1080/1369118X.2022.2161830

Akter, S., Dwivedi, Y. K., Sajib, S., Biswas, K., Bandara, R. J., & Michael, K. (2022). Algorithmic bias in machine learning-based marketing models. Journal of Business Research, 144, 201-216. https://doi.org/10.1016/j.jbusres.2022.01.083

Cao, H. H., Ma, L., Ning, Z. E., & Sun, B. (2024). How does competition affect exploration vs. exploitation? a tale of two recommendation algorithms. Management Science, 70(2), 1029-1051. https://doi.org/10.1287/mnsc.2023.4722

Chen, N. (2022). Research on E-Commerce Database Marketing Based on Machine Learning Algorithm. Computational Intelligence and Neuroscience, 2022. https://doi.org/10.1155/2022/7973446

Cook, J., Davies, K., Farrugia, D., Threadgold, S., Coffey, J., Senior, K., … & Shannon, B. (2023). Buy now pay later services as a way to pay: credit consumption and the depoliticization of debt. Consumption Markets & Culture, 26(4), 245-257. https://doi.org/10.1080/10253866.2023.2219606

De Best, R. (2024). Estimated transaction value of buy now, pay later (BNPL) in the United Kingdom (UK) in 2023, with forecasts for 2024 and 2029. Statista. https://www.statista.com/statistics/1372750/bnpl-transaction-value-in-uk/

de Marcellis-Warin, N., Marty, F., Thelisson, E., & Warin, T. (2022). Artificial intelligence and consumer manipulations: from consumer’s counter algorithms to firm’s self-regulation tools. AI and Ethics, 2(2), 259-268. https://doi.org/10.1007/s43681-022-00149-5

How does Klarna really work? (2024). klarna.com. https://www.klarna.com/uk/blog/how-does-klarna-really-work/

Kamau, N., & Dehoky, D. (2021). Personalizing the post-purchase experience in online sales using machine learning. https://www.diva-portal.org/smash/record.jsf?pid=diva2%3A1670801&dswid=-8032

Kotras, B. (2020). Mass personalization: Predictive marketing algorithms and the reshaping of consumer knowledge. Big data & society, 7(2), 2053951720951581. https://doi.org/10.1177/2053951720951581

Li, X., Rong, Y., Zhang, R. P., & Zheng, H. (2022). Online advertisement allocation under customer choices and algorithmic fairness. Forthcoming at Management Science. https://dx.doi.org/10.2139/ssrn.3538755

Liu, Z., Sockin, M., & Xiong, W. (2023). Data privacy and algorithmic inequality (No. w31250). National Bureau of Economic Research. https://doi.org/10.3386/w31250

Park, E. S. & Park, M. S. (2020). Factors of the Technology Acceptance Model for Construction IT. Applied Sciences, 10(22), 8299. https://doi.org/10.3390/app10228299

Pavlidou, V., Otterbacher, J., & Kleanthous, S. (2022, December). Fairness Issues in Algorithmic Digital Marketing: Marketers’ Perceptions. In European, Mediterranean, and Middle Eastern Conference on Information Systems (pp. 319-338). Cham: Springer Nature Switzerland. https://doi.org/10.1007/978-3-031-30694-5_24

Pellandini-Simányi, L. (2023). Algorithmic classifications in credit marketing: How marketing shapes inequalities. Marketing Theory, 14705931231160828. https://doi.org/10.1177/14705931231160828

Shop and pay the klarna way. (2024). Klarna UK. . https://www.klarna.com/uk/how-klarna-works/

Srinivasan, R., & Sarial-Abi, G. (2021). When algorithms fail: Consumers’ responses to brand harm crises caused by algorithm errors. Journal of Marketing, 85(5), 74-91. https://doi.org/10.1177/0022242921997082

Explore Recent Blogs

-

How to Write a Detailed Report: From Planning to Polishingby arora.vijay27jan on January 29, 2026

A detailed report represents critical research and professional competency. Reports provide readers with a comprehensive understanding of the information presented in a coherent format. In addition to reporting the details of a specific situation or… The post How to Write a Detailed Report: From Planning to Polishing first appeared on Digi Assignment Help.

-

How to Write an Assignment on the First Pageby arora.vijay27jan on January 13, 2026

Mastering the skill of writing assignments is one of the most essential academic skills for every student. While most focus on what is contained in the body of the assignment, students frequently overlook the significance… The post How to Write an Assignment on the First Page first appeared on Digi Assignment Help.

-

Most Controversial Debate Topics To Win Any Argumentby arora.vijay27jan on January 12, 2026

Debates are not simply casual conversations about what you think or feel on a specific subject, but rather well-organised and structured forms of discourse in which opposing sides analyse and defend their respective opinions, using… The post Most Controversial Debate Topics To Win Any Argument first appeared on Digi Assignment Help.

-

Significance Of Report Writingby arora.vijay27jan on January 9, 2026

The report is an important part of academic and professional life because it allows individuals to document information systematically, clearly, and indiscriminately so readers can make informed decisions about how to utilise that information for… The post Significance Of Report Writing first appeared on Digi Assignment Help.

-

How to Write a Hypothesis? Step-by-Step Guide with Examplesby Amelia on January 2, 2026

Many students must have experienced the “appear or disappear” situation when formulating a hypothesis for a new research venture. You are certainly not alone if you embark on a new research project and are unsure… The post How to Write a Hypothesis? Step-by-Step Guide with Examples first appeared on Digi Assignment Help.

-

How to Choose the Right Nursing Topic for Your Final-Year Projectby Amelia on July 8, 2025

Nursing is a competitive course offering a promising career for students. It is rigorous and demands up to date knowledge of the subject, good assignment writing, and field practice. Hence scoring good marks in nursing… The post How to Choose the Right Nursing Topic for Your Final-Year Project first appeared on Digi Assignment Help.